Get Started - Tingg Advance Pay (TAP)

API Description for Tingg Advance Pay - Supply Finance Chain

Problem Statement

Based on most corporate supply chain policies, suppliers often receive payments for invoices in a period of between 60-90 days. This causes these pain points to the main actors in the supply-chain ecosystem:

- The supplier: Faces operational challenges as they need to wait between 60-90 days to get paid. It also takes up to 7 days or more to receive financing due to a lot of paperwork needed.

- The corporate buyer: Supply disruption impacts the buyer when the supplier is facing cash flow problems

- The bank: Bank onboarding process of a merchant is cumbersome and could take up to 3+ weeks.

- The Sponsor: Unavailable automated system to process supply chain financing and scale it across the continent

Proposed Solution

The proposed solution is to build a supply chain invoicing discounting solution within tingg to enable suppliers to receive early payments against their invoices.

This is a solution that allows buyers to pay their suppliers upon delivery and submission of invoices at a discount.

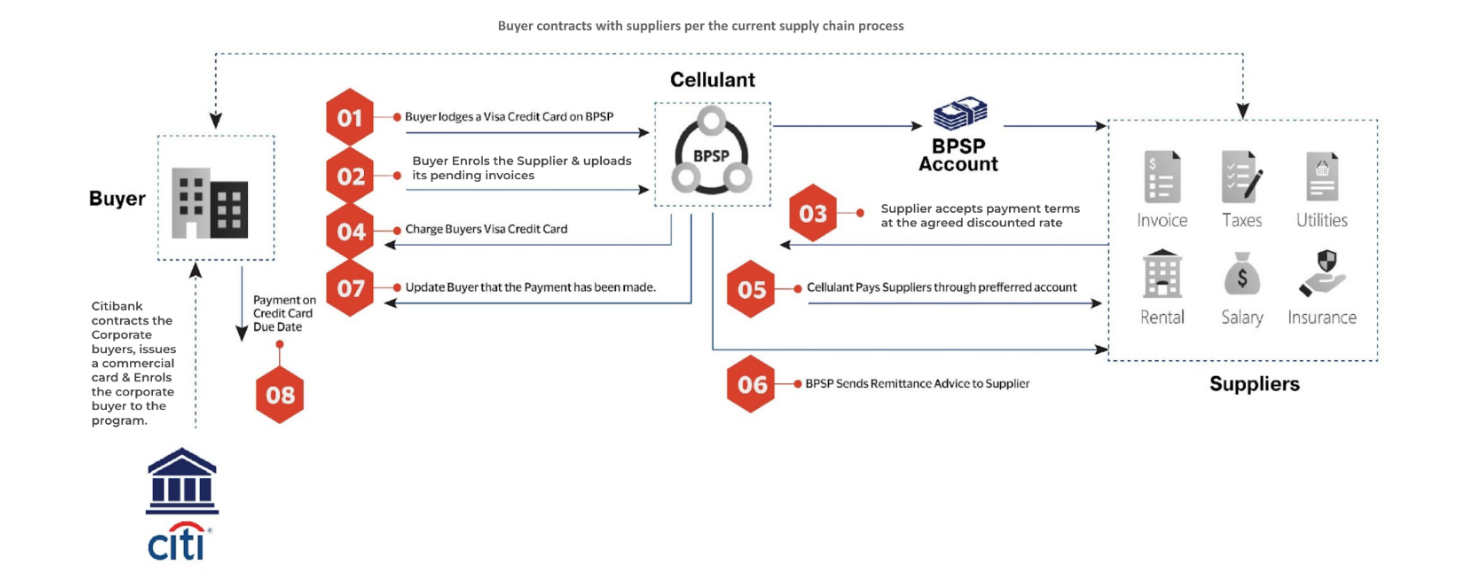

The image below illustrates the proposed journey through which an invoice will go through from the moment its initialized to the moment its fulfilled:

The solution will have different capabilities as below:

- Onboarding Module

a) Supplier Onboarding

b) Buyer/Corporate onboarding

c) Acquirer/Bank onboarding

d) Visa/Sponsor onboarding - Invoice Management module

a) Invoice creation and verification

b) Buyer and supplier verification

c) Supplier acceptance - Card management module

a) Manage the corporate or buyer credit card - Reporting module

a) Allow easy management of invoices

b) Tracking the processing of invoices and cash disbursements to suppliers

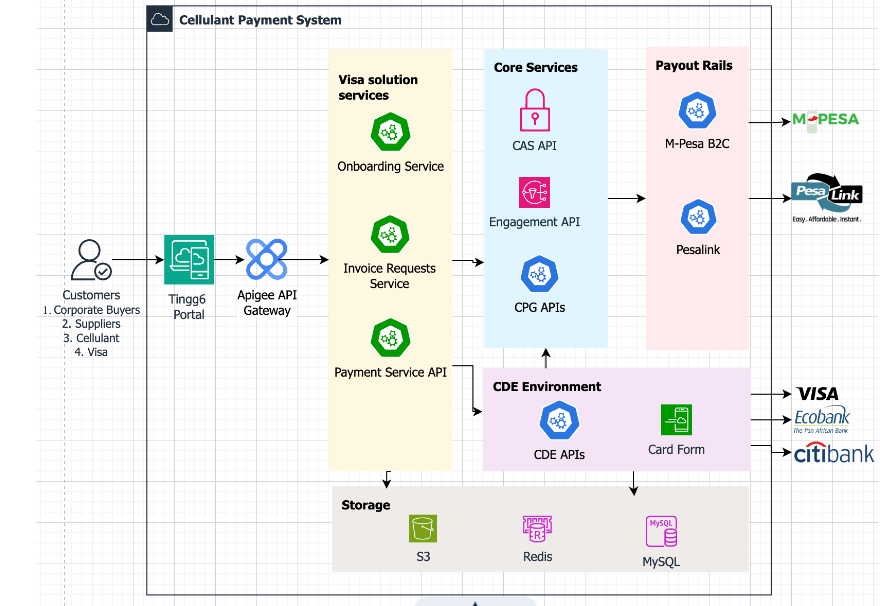

System Architecture

The Visa Supply Chain discounting platform will provide a centralised platform for all related activities by the supplier, buyer/corporate, acquirer/bank and visa/sponsor.

Below is an overview of the different components and how they interact with each other:

High-Level Architecture

Components and Modules

The Visa Supply Chain Invoice Discounting solution project is broken down into 5 modules:

-

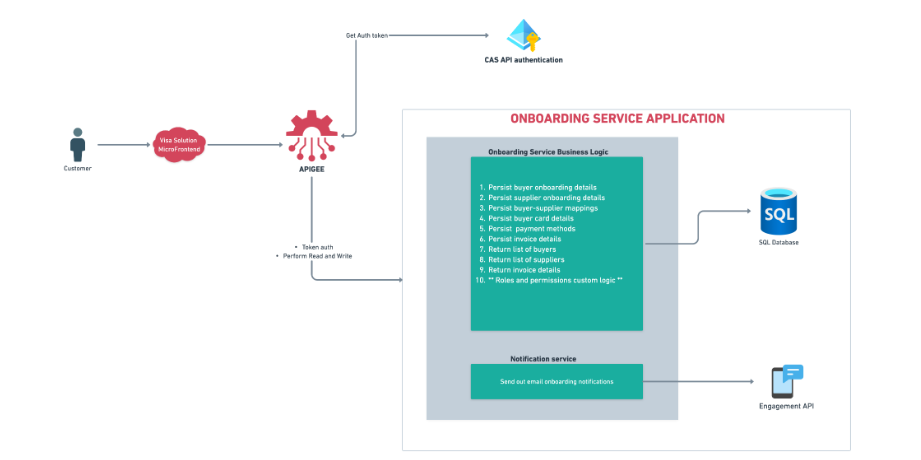

Onboarding module

The onboarding module primarily serves to onboard the supplier to the tingg platform. In addition to this, it serves to:

a. Configure and persist Buyer details.

b. Persist the mappings between the sponsor, financier, buyer and supplier.

c. Persist the payment methods(details where the money will be terminated to) of the supplier.

The below diagram is a high-level architecture diagram showing the interactions of the components.

As a pre-requisite to the onboarding of the supplier, the Sponsor, Financier and Buyer need to be onboarded. This will be done through the normal process for onboarding by Cellulant.

For future iterations of the product, the financiers will onboard the buyers before the suppliers are onboarded.

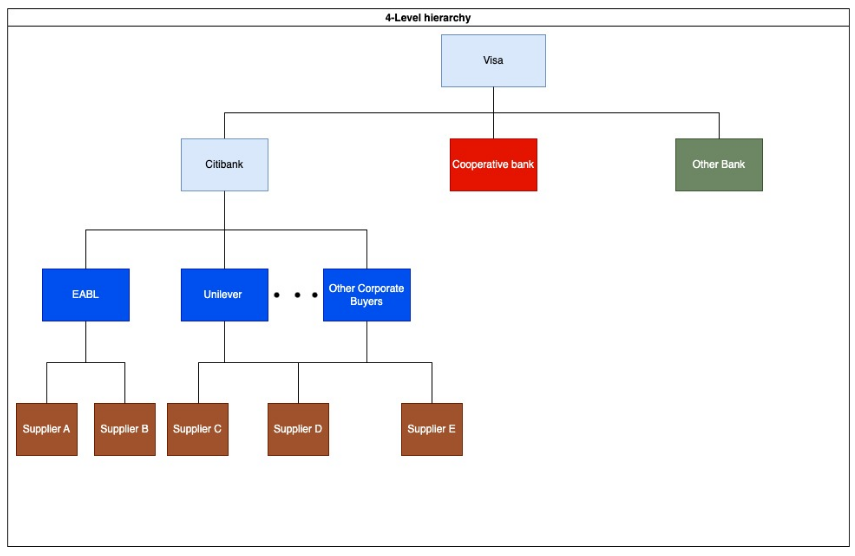

The below diagram is a hierarchical representation of the various personas in the ecosystem.

-

Invoice Management Module

This module will be used by buyers to manage supplier invoices. The buyer will, key-in and submit a supplier invoice, which will then be validated and saved in the system. Supplier will be notified about the invoice discounting offer for confirmation. Once accepted by the supplier, the buyer will be notified of the acceptance and the system will proceed to charge the buyer’s card and disburse funds to the supplier. The buyer and the supplier can view the status of the payouts in the system -

Card Management Module

This module allows buyers to add, activate and deactivate a card. The card details are processed through a PCI-DSS compliant standards. Maker-Checker functionality is implemented when adding, activating and deactivating the card to curb fraudulent cases. -

Payment Module

This module is responsible for the charging of the card and disbursement of the funds to the supplier payment methods. Once an invoice has been acknowledged by the supplier, the card is charged and money is transferred from the buyer to Cellulants collection account.

The treasury team will then receive a notification to check whether money has been credited to Cellulant’s collection account. They will then credit Cellulant’s Payouts account before releasing the funds to be disbursed.

Money can be processed through 3 channels:

a). Real-time Gross Settlement(RTGS): This will be for transactions above KES 999,999. For the MVP this mode will be disabled until the payment rail is developed and ready.

b). Pesalink Instant Bank Transfer: This is for amounts between and inclusive of KES 10 and KES 999,999.

c). Mobile Money: This is for amounts between KES 10 and KES 500,000.

-

Reporting Module

This module avails reports to the sponsor, financiers(banks), buyers and suppliers. These reports include;

a. Onboarding reports: These are reports of the child clients that the visa/sponsor, acquirer/banks or corporates/buyer have onboarded into the system.

b. Invoices reports: These are the reports of the invoices uploaded to the system by the buyers for the suppliers. These reports will show the status of the invoices, whether pending supplier confirmation or pending payout or paid.

c. Payment reports: These reports show the status of the payments initiated in the system to the suppliers.

Updated 23 days ago